Retirement Planning in India 2025: How to Build a Secure Future and Beat Inflation

Introduction

Retirement planning is no longer just a choice — it’s a necessity for financial freedom in India. With rising inflation, longer life expectancy, and evolving lifestyles, planning early helps you build a strong and secure corpus for a stress-free future.

Whether you’re in your 20s or 50s, understanding your post-retirement income needs is key to maintaining your lifestyle even after your regular earnings stop.

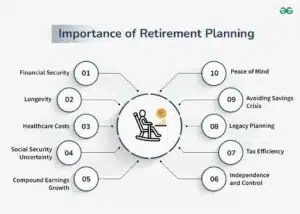

📈 Why Retirement Planning Matters in 2025

India’s economic and demographic trends show a clear shift — people are living longer, healthcare costs are rising, and inflation continues to erode savings. Without proper retirement planning, even a ₹1 crore corpus may fall short in the coming decades.

A solid plan ensures:

- Financial security after your working years

- Peace of mind for you and your family

- Inflation protection through smart investments

- Tax benefits under various schemes and sections

💼 Steps to Build a Strong Retirement Plan

1. Set Clear Financial Goals

Estimate your post-retirement monthly expenses. Multiply by 12 months and account for inflation over 20–25 years.

2. Start Early and Stay Consistent

The earlier you start, the more compounding works in your favor. A 25-year-old investing ₹10,000 monthly can accumulate much more than someone starting at 35.

3. Diversify Your Investments

Mix equity, mutual funds, NPS, PPF, and fixed income instruments to balance risk and return.

4. Account for Inflation

Always calculate your future corpus value based on at least 6–7% inflation rate.

The earlier you start, the more compounding works in your favor. A 25-year-old investing ₹10,000 monthly can accumulate much more than someone starting at 35.

5. Review and Adjust Regularly

Track your portfolio annually. Modify your investment mix based on market performance and life goals.

💰 Best Retirement Investment Options in India

- National Pension System (NPS) – Long-term tax-efficient retirement savings.

- Employee Provident Fund (EPF) – Reliable corpus builder for salaried professionals.

- Mutual Funds (Equity & Hybrid) – For higher growth and inflation beating returns.

- Public Provident Fund (PPF) – Stable and safe for long-term accumulation.

- Annuity Plans & Pension Schemes – Provide guaranteed income post-retirement.

🏦 Government & Official Financial Planning Sites (India)

- National Pension System (NPS) – https://www.npscra.nsdl.co.in

- Employees’ Provident Fund Organisation (EPFO) – https://www.epfindia.gov.in

- Public Provident Fund (PPF) – https://www.ppf.in

🧠 Expert Tips for a Secure Future

- Increase your SIP amount annually with income growth.

- Avoid withdrawing from your retirement savings prematurely.

- Include health insurance to safeguard your savings.

- Aim for at least 70–80% of your current income as retirement income.

🕰️ Conclusion

Retirement planning is your roadmap to a financially independent and stress-free life. The earlier you begin, the better your future will look. Make 2025 the year you take charge of your financial destiny — invest smartly, plan wisely, and secure your golden years today.

❓ FAQ Section (FAQ Schema Optimized)

1. Is ₹1 crore enough for retirement in India?

No, ₹1 crore may not be sufficient due to rising inflation and healthcare costs. Experts recommend building a corpus of ₹3–5 crore for a comfortable lifestyle in metro cities by 2045.

2. At what age should I start retirement planning?

The earlier, the better. Ideally, start in your 20s or 30s to maximize the power of compounding. Even small monthly investments grow significantly over 25–30 years.

3. What are the best retirement investment options in India?

Top options include NPS (National Pension System), EPF, PPF, mutual funds (equity & hybrid), and annuity plans. A diversified portfolio helps balance risk and returns.

4. How much should I save for retirement monthly?

It depends on your current age, expected retirement age, and lifestyle. A common rule is to invest 15–20% of your monthly income, increasing yearly as your income grows.

5. How do I protect my retirement corpus from inflation?

Invest in inflation-beating instruments like equity mutual funds, NPS, and hybrid funds. Regularly review your portfolio and adjust asset allocation to maintain real returns.

6. Can I rely only on EPF and PPF for retirement?

EPF and PPF provide stability but may not fully beat inflation. Combining them with equity investments and mutual funds ensures higher corpus growth and financial security.